As business energy consultants, we are constantly on the lookout for the finest deals on the market for our clients, and we work tirelessly to achieve these. Our monthly market reports provide views directly from our specialists. Use our price analysis, market signals, and political changes to help you make the right choice when it comes to energy decisions.

Download PDFDisclaimer: The information contained in this document has been prepared in good faith by Ginger Energy and provides our views on current/future trends and outcomes, but, as with all forecasts dependent upon multiple, complex variables, there is no certainty whatsoever that our forecasts will turn out to be correct. The information may be based on licenced 3rd party data, publicly available sources, assumptions, and observable market conditions and may change without notice. No warranty, express or implied, is made as to the accuracy, correctness, fitness for purpose, completeness or adequacy of this information nor is it intended to serve as basis for any procurement decision and as such Ginger Energy shall not accept any responsibility or liability for any action taken, financial or otherwise, as a result of this information. Please note that this email is intended for the recipient only and may not be copied, reproduced, or distributed without the prior consent of Ginger Energy.

Market Context

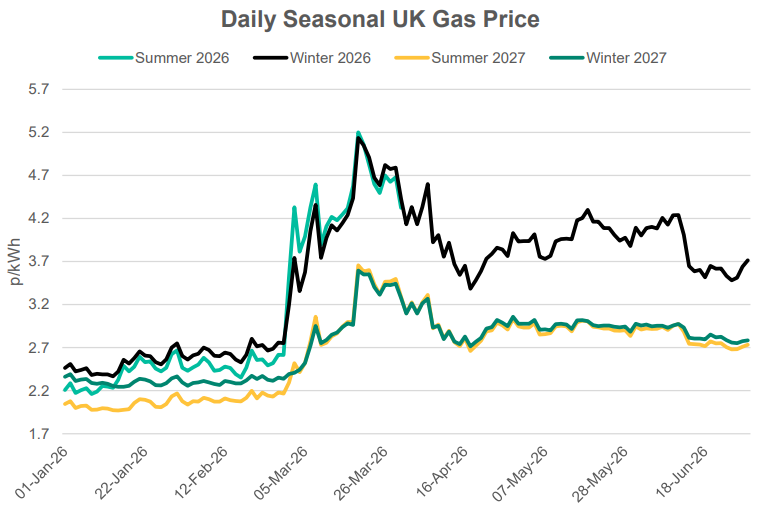

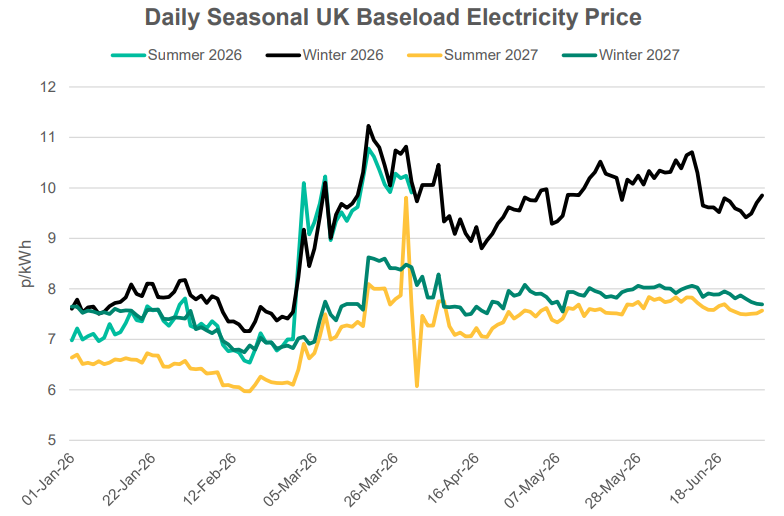

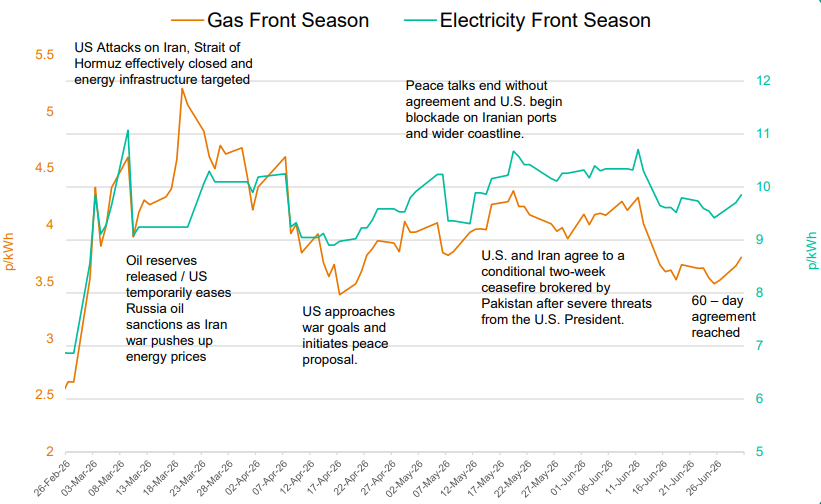

UK gas and power curve prices moved lower across June, although the month was volatile and highly sensitive to Middle East headlines. Front season gas initially rose by around 6% as US-Iran strikes and uncertainty around the Strait of Hormuz supported forward prices. The tone then softened sharply, with front season gas falling around 18% from its early-June high as the market priced in a potential peace agreement, gradual reopening of Gulf shipping, falling oil prices, improving Norwegian supply and weaker demand. Prices recovered slightly into month-end but still finished around 11% below where they started the month.

- Early in the month, fresh US-Iran hostilities revived risk premium, with forward gas and power supported by uncertainty over Gulf LNG flows, shipping safety and oil-linked sentiment.

- Mid-month prices fell sharply after President Trump suggested an end to the Iran war was close, raising expectations that the Strait of Hormuz, the key Gulf shipping route for oil and LNG, could reopen if a deal was confirmed.

- Later in June, prices rebounded slightly as initial optimism around a peace deal faded after the US and Iran exchanged attacks despite previously agreeing to stop hostilities, increasing skepticism over whether a lasting agreement could be reached.

- Norwegian supply improved as maintenance and technical issues eased at assets including Troll, a major Norwegian gas field in the North Sea, helping loosen the UK balance and supporting storage injections.

- Prompt prices also softened over the month, with NBP spot gas and UK baseload power averages falling month-on-month as warmer weather, stronger renewable output at times and improving supply reduced near-term tightness.

- By late June, European gas storage was around 49% full, versus a five-year average of 60%. At the current pace of injections, storage levels are on track to reach only 70–75% by the end of summer, remaining below the 83% pre-winter target agreed for winter 2025.

- A confirmed US-Iran peace deal would reduce geopolitical risk premium across gas, power and oil markets.

- Improving Norwegian pipeline supply would support UK and European storage injections.

- Softer summer demand and stronger renewable output would reduce gas-for-power requirements.

- European gas storage remains below normal, leaving winter contracts exposed to any slowdown in injections.

- Delays to reopening the Strait of Hormuz would keep LNG availability and shipping risk priced into the curve.

- Stronger Asian summer LNG demand could divert flexible cargoes away from Europe.

In Other News

Extreme heat increased electricity demand across Europe as cooling load rose, highlighting the growing summer risk from heatwaves and their potential to tighten power balances when renewable output or grid availability is constrained.

Seasonal Prices

Price Table

Prices generally moved lower month-on-month as geopolitical risk premium unwound and supply conditions improved. Power followed gas lower across most forward products, although the front-month power contract was broadly unchanged.

Month End Energy Only Prices

Spot Prices

| Fuel | June-26 (p/kWh) | May-26 (p/kWh) | Month-on-Month Difference |

|---|---|---|---|

| Gas (NBP) | 3.73 | 4.01 | -7% |

| Power (UK Baseload) | 10.15 | 10.42 | -3% |

Front Months

| Fuel | June-26 (p/kWh) | May-26 (p/kWh) | Month-on-Month Difference |

|---|---|---|---|

| Gas (NBP) | 3.59 | 3.90 | -8% |

| Power (UK Baseload) | 9.95 | 9.95 | 0% |

Front Season

| Fuel | June-26 (p/kWh) | May-26 (p/kWh) | Month-on-Month Difference |

|---|---|---|---|

| Gas (NBP) | 3.71 | 3.88 | -4% |

| Power (UK Baseload) | 9.85 | 10.06 | -2% |

Annual Price (Oct-26)

| Fuel | April-26 (p/kWh) | May-26 (p/kWh) | Month-on-Month Difference |

|---|---|---|---|

| Gas (NBP) | 3.42 | 3.57 | -4% |

| Power (UK Baseload) | 8.83 | 8.96 | -2% |

Outlook

The curve is likely to remain driven by whether geopolitical de-escalation translates into physical supply normalisation. A confirmed and durable reopening of the Strait of Hormuz, especially if Qatari LNG flows recover and European storage injections remain steady, could add bearish pressure. However, any downside will be limited while European storage remains below seasonal norms and shipping, insurance, sanctions and security risks continue to affect Gulf cargo movements. Norwegian maintenance, Asian LNG demand, summer weather and oil-market tightness remain the main forward risks.

Bearish Signals

Bullish Signals

Middle East Conflict Update

- The war began in late February, triggering an effective closure of the Strait of Hormuz, the key Gulf route for oil and LNG, and a sharp rise in front-season gas on Qatari LNG supply concerns.

- Front-season gas prices doubled at one stage, before easing as US and allied statements sought to calm markets and support safe passage through the Strait.

- By early April, some risk premium unwound as President Trump suggested the

US campaign could be nearing an end, with front-season gas falling around 13%

in one session.

Recent Events

- Through May and early June, prices remained headline-driven, with peace-deal optimism pulling prices lower and renewed attacks quickly rebuilding risk premium.

- In mid-June, the US and Iran signed a preliminary 60-day ceasefire intended to reopen the Strait of Hormuz, while harder issues were deferred to later talks.

- The deal softened oil and European gas prices but did not trigger a major fall in front-season gas as markets had already priced in a high chance of de-escalation.

- The agreement remains fragile, with the US and Iran exchanging fresh attacks after agreeing to stop hostilities, raising doubts over whether the ceasefire can hold.

- Iranian officials not attending the latest Doha meetings adds further uncertainty around shipping rules, sanctions, nuclear issues and regional security.

- Strait of Hormuz flows have not meaningfully normalised, with mine clearance, tanker backlogs, supply-chain disruption and shipping caution still limiting movements.

- Future Risk: Further risk-premium reductions may be limited until markets see sustained vessel movements and clear evidence that Qatari LNG exports are recovering.

- As summer progresses, weak European storage increases the risk of renewed bullishness if a durable agreement and stronger Gulf flows do not materialise.

- The key risk is shifting from headline risk to delivery risk: prices are likely to stay supported until physical flows and storage injections improve.

Future Risk

Price movement since the war began

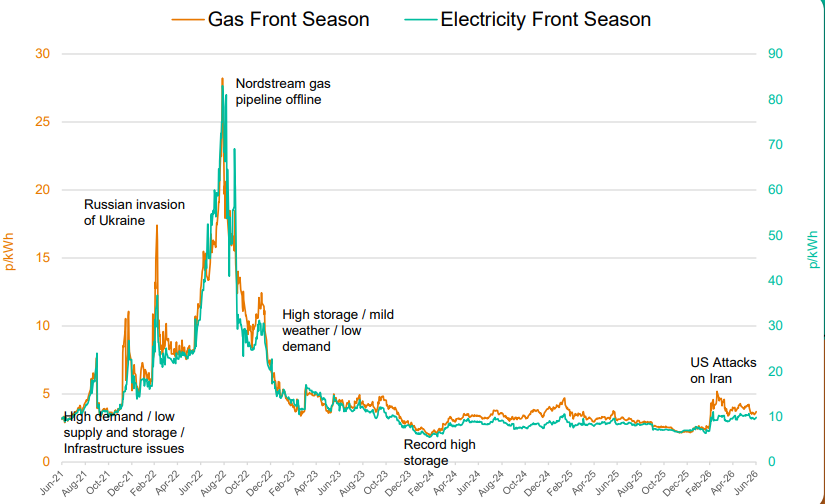

Wider Historical Context

Want the best energy and water contracts for your business?

Get in touch today to start saving money and time spent on finding the best business energy deals.