As business energy consultants, we are constantly on the lookout for the finest deals on the market for our clients, and we work tirelessly to achieve these. Our monthly market reports provide views directly from our specialists. Use our price analysis, market signals, and political changes to help you make the right choice when it comes to energy decisions.

Download PDFDisclaimer: The information contained in this document has been prepared in good faith by Ginger Energy and provides our views on current/future trends and outcomes, but, as with all forecasts dependent upon multiple, complex variables, there is no certainty whatsoever that our forecasts will turn out to be correct. The information may be based on licenced 3rd party data, publicly available sources, assumptions, and observable market conditions and may change without notice. No warranty, express or implied, is made as to the accuracy, correctness, fitness for purpose, completeness or adequacy of this information nor is it intended to serve as basis for any procurement decision and as such Ginger Energy shall not accept any responsibility or liability for any action taken, financial or otherwise, as a result of this information. Please note that this email is intended for the recipient only and may not be copied, reproduced, or distributed without the prior consent of Ginger Energy.

Market Context

Seasonal prices retreated slightly from highs in late January as milder weather eased supply concerns amid growing geopolitical tensions. Negotiations between the US and Iran regarding Iran’s nuclear program and further peace talks between Ukraine and Russia failed to deliver any meaningful results which has kept tension in the markets despite the more positive fundamental outlook due to warmer weather forecasts.

- Talks between the US and Iran regarding Iran’s nuclear program took place through the month with no clear breakthrough and escalating rhetoric from both sides.

- In a response to growing US Military presence in the Middle East, Iran announced a temporary, partial closure of the Strait of Hormuz for military exercises Causing prices to rise sharply after descending for much of the month.

- Ukraine and Russia peace talks once again ended with no significant progress and territory continuing to be the main area of contention.

- LNG flows to Europe remained strong through the month as a Greek joint venture finalised plans to supply US LNG to Ukraine starting in March 2026 via transit through Bulgaria, Romania, and Moldova.

- Both milder weather and warmer future forecasts reduced immediate pressure on storage.

- EU gas storage was at 30% at the end of February, 13% lower than the 5-year average, however, the warmer conditions are reducing the immediate pressure and have even permitted injections in Germany where storage levels were particularly low.

- Mild weather forecasts for Northwest Europe.

- A ceasefire between US/Israel and Iran and local proxies and resumption of maritime traffic through the Strait of Hormuz.

- Continued disruption impacting flows of oil, gas, and LNG through the Strait of Hormuz.

- Wider escalation of the current conflict throughout the Middle East or beyond.

In Other News

From 1st April a new price cap will come into effect in the UK. Energy prices will go down by around £117 or 7% for a typical household who use electricity and gas. Much of the reductions due to the removal of government policy costs have been eroded by higher network charges.

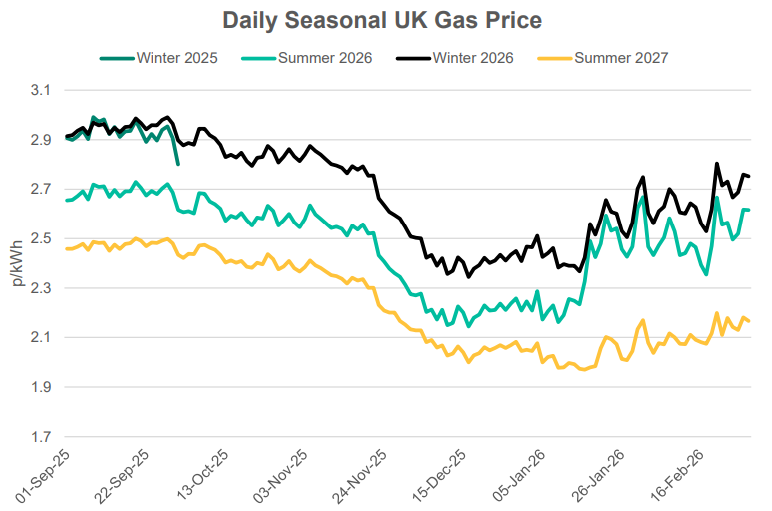

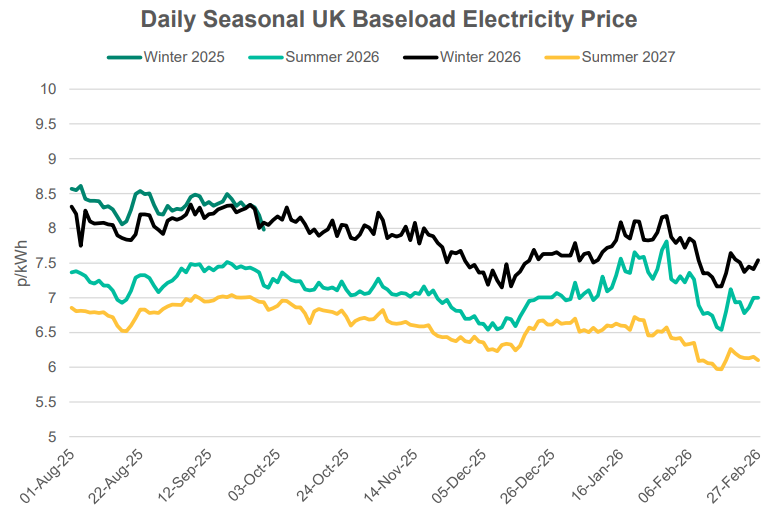

Seasonal Prices

Price Table

Front month prices saw the largest declines in February. The impending end to the winter season and milder weather forecast drove the declines. Seasonal prices have been less impacted as low storage means Europe is set for a busy summer injection season.

Month End Energy Only Prices

Spot Prices

| Fuel | February-26 (p/kWh) | January-26 (p/kWh) | Month-on-Month Difference |

|---|---|---|---|

| Gas (NBP) | 2.72 | 3.06 | -11% |

| Power (UK Baseload) | 8.02 | 9.60 | 28% |

Front Months

| Fuel | February-26 (p/kWh) | January-26 (p/kWh) | Month-on-Month Difference |

|---|---|---|---|

| Gas (NBP) | 2.71 | 3.55 | -24% |

| Power (UK Baseload) | 7.50 | 10.59 | -29% |

Front Season

| Fuel | February-26 (p/kWh) | January-26 (p/kWh) | Month-on-Month Difference |

|---|---|---|---|

| Gas (NBP) | 2.62 | 2.67 | -2% |

| Power (UK Baseload) | 7.00 | 7.81 | -10% |

Annual Price (Apr-26)

| Fuel | February-26 (p/kWh) | January-26 (p/kWh) | Month-on-Month Difference |

|---|---|---|---|

| Gas (NBP) | 2.71 | 2.73 | -1% |

| Power (UK Baseload) | 7.30 | 8.01 | -9% |

Outlook

Mild weather forecast provide a small amount of good news for prices as we edge out of winter but events unfolding in the Middle East are going to drive market sentiment in the coming weeks. If the Strait of Homuz continues to be closed to cargoes, then supply will be impacted in a market that was already dealing with thin global supply and demand margins. The majority of LNG from the region finds a home in Asia rather than Europe but buyers will now be required to source elsewhere increasing global competition and keeping prices elevated.

Bearish Signals

Bullish Signals

Want the best energy and water contracts for your business?

Get in touch today to start saving money and time spent on finding the best business energy deals.