As business energy consultants, we are constantly on the lookout for the finest deals on the market for our clients, and we work tirelessly to achieve these. Our monthly market reports provide views directly from our specialists. Use our price analysis, market signals, and political changes to help you make the right choice when it comes to energy decisions.

Download PDFDisclaimer: The information contained in this document has been prepared in good faith by Ginger Energy and provides our views on current/future trends and outcomes, but, as with all forecasts dependent upon multiple, complex variables, there is no certainty whatsoever that our forecasts will turn out to be correct. The information may be based on licenced 3rd party data, publicly available sources, assumptions, and observable market conditions and may change without notice. No warranty, express or implied, is made as to the accuracy, correctness, fitness for purpose, completeness or adequacy of this information nor is it intended to serve as basis for any procurement decision and as such Ginger Energy shall not accept any responsibility or liability for any action taken, financial or otherwise, as a result of this information. Please note that this email is intended for the recipient only and may not be copied, reproduced, or distributed without the prior consent of Ginger Energy.

Market Context

April was another volatile month for energy markets, with front season gas prices ending 9% lower than at the end of March despite sharp movements during the period. Prices fell by around 20% mid-month on hopes of progress towards a longer-term peace agreement, before retracing some of those losses as negotiations became more uncertain and the Strait of Hormuz remained effectively closed, prolonging disruption to global supply.

- The month began with optimism that the conflict could be nearing an end after the U.S. President suggested the U.S. was “nearly done”, prompting oil and gas prices to fall.

- Prices then moved higher in the first week of the month after the U.S. threatened further action against Iranian infrastructure, including power plants and bridges, attempting to force progress towards a ceasefire.

- The U.S. and Iran agreed to a conditional two-week ceasefire brokered by Pakistan, although the terms remained contentious and there was uncertainty over whether Lebanon was included.

- Both sides claimed victory, with the U.S. stating it had achieved and exceeded its war objectives, while Iran framed the survival of the regime and completion of its stated objectives as a success.

- Pakistan invited both sides to further talks in Islamabad as efforts continued to turn the temporary ceasefire into a longer-lasting agreement and despite prolonged negotiations, a formal agreement was not reached, causing gas prices to rise as confidence in a lasting settlement weakened.

- The U.S. President increased focus on the Strait of Hormuz, confirming that a blockade of Iranian ports would begin, while U.S. Central Command said it would not impede vessels travelling through the Strait to or from other countries.

- By the end of the month, the fragile ceasefire remained in place despite reports of further attacks in the Strait of Hormuz, keeping geopolitical risk firmly priced into the market.

- Brent crude reached its highest level since the start of the conflict on the final day of April, rising above $125/bbl before closing the month nearer $115/bbl.

- European gas storage ended April at 32%, below the five-year average of 43%, with strong global LNG competition slowing the start of the injection season as high prices weigh on the economics of filling storage.

- Falling heating demand as temperatures rise into the storage injection season.

- Any meaningful reopening of the Strait of Hormuz would ease supply concerns.

- Diplomatic progress or a lasting ceasefire could reduce geopolitical risk premium.

- Continued disruption to maritime traffic through the Strait of Hormuz would prolong global supply uncertainty.

- A prolonged diplomatic impasse could keep geopolitical risk elevated.

- Higher Asian demand could increase LNG competition and support prices further out on the curve.

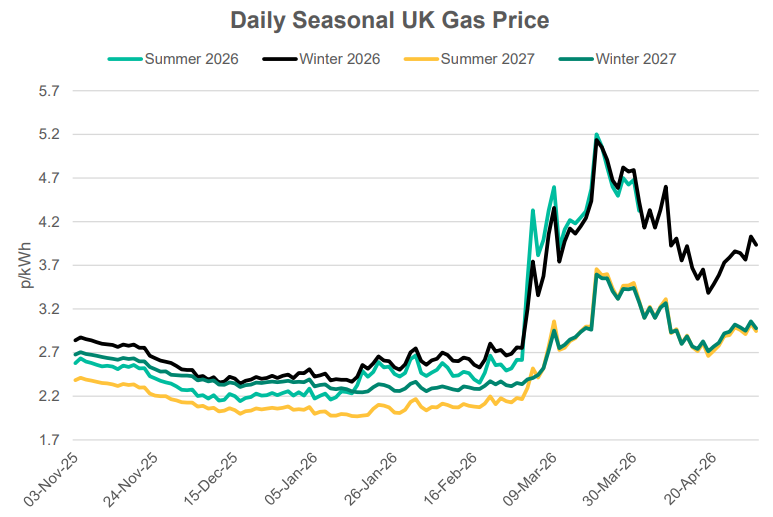

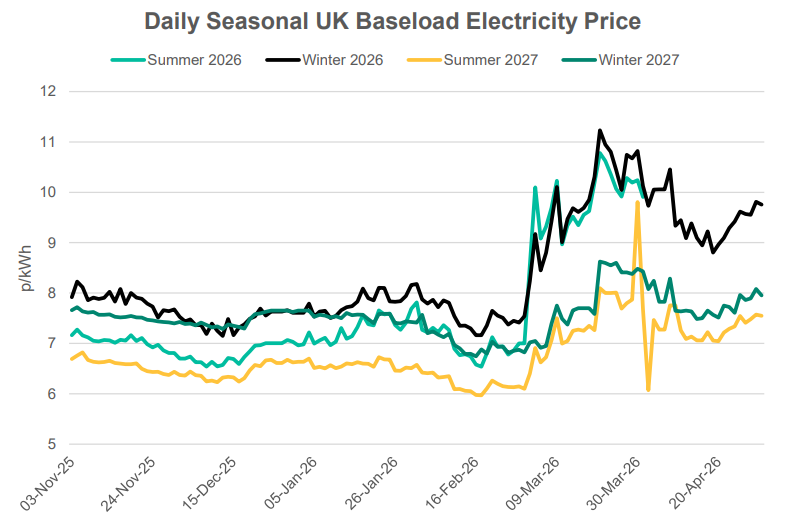

Seasonal Prices

Price Table

Prices generally softened through April although losses were curbed as initial optimism from the ceasefire agreement subsided when talks failed to lead to any meaningful lasting agreement. Spot, Front Month, and Front Season gas prices are currently closely aligned with lower price levels only being witnessed from Summer-27 showing that risk is being more concentrated in the short to medium term.

Month End Energy Only Prices

Spot Prices

| Fuel | April-26 (p/kWh) | March-26 (p/kWh) | Month-on-Month Difference |

|---|---|---|---|

| Gas (NBP) | 3.84 | 4.49 | -14% |

| Power (UK Baseload) | 8.80 | 9.89 | -11% |

Front Months

| Fuel | April-26 (p/kWh) | March-26 (p/kWh) | Month-on-Month Difference |

|---|---|---|---|

| Gas (NBP) | 3.86 | 4.34 | -11% |

| Power (UK Baseload) | 9.38 | 9.51 | -1% |

Front Season

| Fuel | April-26 (p/kWh) | March-26 (p/kWh) | Month-on-Month Difference |

|---|---|---|---|

| Gas (NBP) | 3.93 | 4.32 | -9% |

| Power (UK Baseload) | 9.76 | 9.91 | -2% |

Annual Price (Apr-26)

| Fuel | April-26 (p/kWh) | March-26 (p/kWh) | Month-on-Month Difference |

|---|---|---|---|

| Gas (NBP) | 3.64 | 4.40 | -17% |

| Power (UK Baseload) | 8.76 | 10.03 | -13% |

Outlook

The fundamental outlook remains broadly bearish, with heating demand expected to fall as markets move further into the storage injection season. However, geopolitical risk is likely to remain the dominant price driver, with focus centered on whether maritime traffic through the Strait of Hormuz resumes in meaningful volumes. Forward markets are also facing additional weather-related risk from forecasts of a strengthening El Niño, which could bring extreme heat and heavy rainfall across parts of Asia. While prices are currently holding relatively steady, a prolonged diplomatic impasse combined with rising weather risk could add upward pressure to already heightened market prices.

Bearish Signals

Bullish Signals

Want the best energy and water contracts for your business?

Get in touch today to start saving money and time spent on finding the best business energy deals.