As business energy consultants, we are constantly on the lookout for the finest deals on the market for our clients, and we work tirelessly to achieve these. Our monthly market reports provide views directly from our specialists. Use our price analysis, market signals, and political changes to help you make the right choice when it comes to energy decisions.

Download PDFDisclaimer: The information contained in this document has been prepared in good faith by Ginger Energy and provides our views on current/future trends and outcomes, but, as with all forecasts dependent upon multiple, complex variables, there is no certainty whatsoever that our forecasts will turn out to be correct. The information may be based on licenced 3rd party data, publicly available sources, assumptions, and observable market conditions and may change without notice. No warranty, express or implied, is made as to the accuracy, correctness, fitness for purpose, completeness or adequacy of this information nor is it intended to serve as basis for any procurement decision and as such Ginger Energy shall not accept any responsibility or liability for any action taken, financial or otherwise, as a result of this information. Please note that this email is intended for the recipient only and may not be copied, reproduced, or distributed without the prior consent of Ginger Energy.

Market Context

Gas and electricity prices have responded sharply to the escalation of conflict in the Middle East, rising rapidly to their highest levels since January 2023. The primary driver of these increases has been the effective closure of the Strait of Hormuz, a critical transit route for approximately 20% of global oil and gas flows. This has significantly disrupted supply dynamics, forcing global buyers to seek alternative sources and increasing competition. The situation has been further exacerbated by damage to major energy infrastructure in the region, intensifying concerns around prolonged supply disruption and reinforcing upward pressure on prices.

- In late February, the United States and Israel initiated a coordinated offensive targeting Iranian assets, prompting a rapid escalation in regional tensions.

- Iran responded with retaliatory strikes across multiple locations in the Middle East, heightening geopolitical risk and market volatility.

- Iran prohibited maritime transit through the Strait of Hormuz with multiple confirmed attacks on vessels. As of the end of March certain parties are being allowed through the Strait, although it remains closed to all US or Israeli allied ships.

- The Ras Laffan LNG facility in Qatar, the world’s largest, sustained significant damage following an Iranian missile strike. The disruption has impacted output with the CEO stating it could take 3–5 years for output capacity to fully recover.

- Additional upward pressure on prices emerged from U.S. threats to Iranian energy infrastructure,coupled with warnings of severe retaliation from Iran, although some of this escalation rhetoric has since moderated.

- Oil markets experienced significant volatility throughout the month, reacting to statements from the U.S. President and the largest ever release of oil reserves by the International Energy Agency. Prices peaked near $120/bbl before closing the month just above $100/bbl.

- A late-month price correction was driven by indications that the U.S. may withdraw from Iran (irrespective of a formal ceasefire agreement) in a matter of weeks, alongside typical end-ofwinter position settling across trading portfolios.

- European gas storage levels ended the winter season at 28%, materially below the five-year average of 37%. This deficit is expected to sustain upward pressure on gas prices over the summer as markets focus on meeting refilling targets. However, high summer prices could inhibit refilling pushing risk further down the curve into next winter and beyond.

- U.S. and Israel ceasing their military operation in the Middle East.

- Increased traffic moving through the Strait of Hormuz.

- Possible prolonging of the war with reports of US troops preparing for a ground invasion.

- The longer the global supply disruption continues the more prices will have to rise to incentivise demand destruction to balance global supply and demand.

In Other News

The closure of the Strait of Hormuz, is expected to have broad cross-commodity impacts beyond energy markets. Disruptions to gas supply — a key input in fertiliser production — are likely to drive higher prices, or worse, shortages. Rising transportation and production costs are expected to feed through into higher food prices and contribute to wider inflationary pressures across global economies.

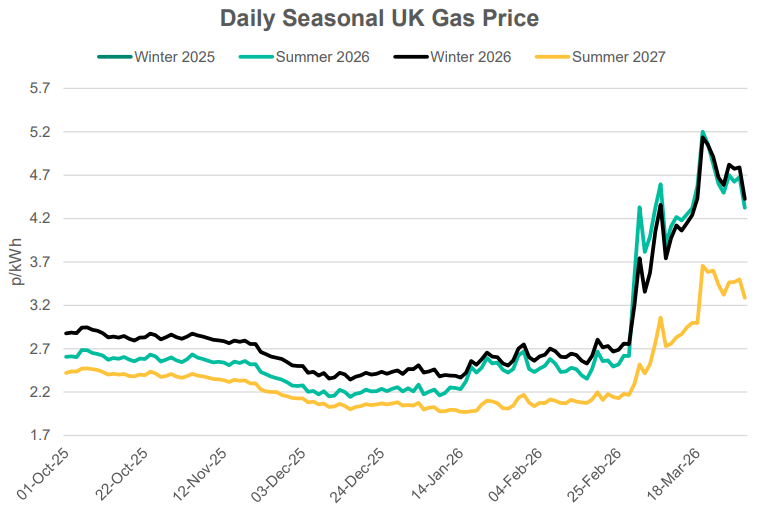

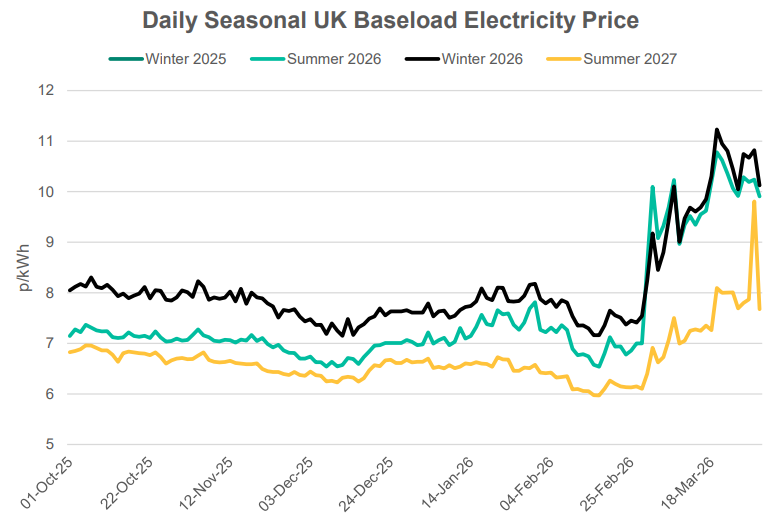

Seasonal Prices

Price Table

Prices have risen along the curve with the impact of the war being felt more acutely on gas prices than power. Nonenergy prices are also increasing adding to pressure on consumers bills. More detailed information will be available later in the month regarding non-energy cost developments.

Month End Energy Only Prices

Spot Prices

| Fuel | March-26 (p/kWh) | February-26 (p/kWh) | Month-on-Month Difference |

|---|---|---|---|

| Gas (NBP) | 4.49 | 2.72 | 65% |

| Power (UK Baseload) | 9.89 | 8.02 | 58% |

Front Months

| Fuel | March-26 (p/kWh) | February-26 (p/kWh) | Month-on-Month Difference |

|---|---|---|---|

| Gas (NBP) | 4.34 | 2.71 | 60% |

| Power (UK Baseload) | 9.51 | 7.50 | 27% |

Front Season

| Fuel | March-26 (p/kWh) | February-26 (p/kWh) | Month-on-Month Difference |

|---|---|---|---|

| Gas (NBP) | 4.32 | 2.62 | 65% |

| Power (UK Baseload) | 9.91 | 7.00 | 42% |

Annual Price (Apr-26)

| Fuel | March-26 (p/kWh) | February-26 (p/kWh) | Month-on-Month Difference |

|---|---|---|---|

| Gas (NBP) | 4.40 | 2.71 | 62% |

| Power (UK Baseload) | 10.03 | 7.30 | 37% |

Outlook

Market focus remains firmly on the progression of the conflict and the status of maritime flows through the Strait of Hormuz. While current signals suggest the U.S.may be moving towards a gradual withdrawal from the region—potentially marking the early stages of a return to more normalised shipping activity—any recovery in transit flows is expected to be slow. Transit will also come at a higher cost due to insurance premiums and the potential tolls to be imposed by the Iranian regime. At the same time, indications that the U.S. could deploy ground forces highlight the risk of further escalation, which contrasts with the more conciliatory tone seen in public messaging. Should the conflict become prolonged, and disruptions to oil and gas exports persist, the resulting supply constraints would be likely to sustain elevated price risk across global energy markets for the foreseeable future.

Bearish Signals

Bullish Signals

Want the best energy and water contracts for your business?

Get in touch today to start saving money and time spent on finding the best business energy deals.