As business energy consultants, we are constantly on the lookout for the finest deals on the market for our clients, and we work tirelessly to achieve these. Our monthly market reports provide views directly from our specialists. Use our price analysis, market signals, and political changes to help you make the right choice when it comes to energy decisions.

Download PDFDisclaimer: The information contained in this document has been prepared in good faith by Ginger Energy and provides our views on current/future trends and outcomes, but, as with all forecasts dependent upon multiple, complex variables, there is no certainty whatsoever that our forecasts will turn out to be correct. The information may be based on licenced 3rd party data, publicly available sources, assumptions, and observable market conditions and may change without notice. No warranty, express or implied, is made as to the accuracy, correctness, fitness for purpose, completeness or adequacy of this information nor is it intended to serve as basis for any procurement decision and as such Ginger Energy shall not accept any responsibility or liability for any action taken, financial or otherwise, as a result of this information. Please note that this email is intended for the recipient only and may not be copied, reproduced, or distributed without the prior consent of Ginger Energy.

Market Context

April saw seasonal prices slide to their lowest levels in a year. Recession fears, expected EU storage target changes, and peace between Ukraine and Russia seemingly edging closer, all provided bearish pressure. The Winter 25 gas price dropped over 20% through the month as warm, sunny weather allowed storage injections to begin at pace.

- Peace talks continued throughout April with President Trump becoming frustrated with the slow progress. By the end of the month a minerals deal was signed between the US and Ukraine which was a prerequisite for any peace deal involving a US security guarantee. President Putin has stated he believes the situation is too complex to solve without direct talks between Russia and Ukraine.

- After 100-days of President Trump’s second term his sweeping trade tariffs continue to create macro-economic repercussions even though many of them were paused to allow for trade deal negotiations to take place.

- Global recession fears, because of the proposed tariffs, led to an expectation of reduced industrial demand and a weakening of the dollar which had a bearish impact on seasonal prices.

- Through April, the expected changes to EU mandated gas storage levels came closer to reality with most believing they will be implemented by mid-May again providing further downward pressure to the market.

- A warm, sunny April reduced pressure on storage allowing injections to begin at pace. April always has potential for cold weather and high demand, so this came as a relief to the market.

- EU aggregated gas storage started being filled at a good rate and is now around 35% full. The current trajectory is in line with 2022 when a strong injection season saw comfortable storage levels reached to manage the winter.

In other news

- Rebel Energy was the latest supplier to cease trading due to what their founder described as a “perfect storm” of rising wholesale costs together with the pressure of the cost-of-living crisis on customers. Around 10,000 businesses and 80,000 domestic properties will be impacted.

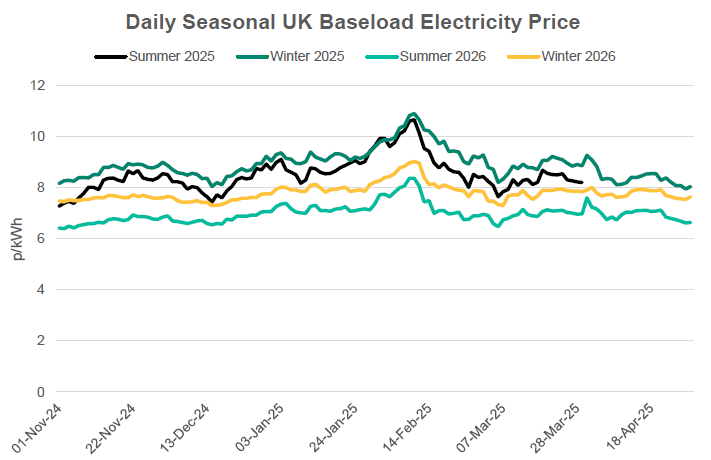

Seasonal Prices

Price Table

Prices dropped across the curve in April with spot gas prices reaching their lowest levels since September 24 and seasonal gas prices dropping to levels not seen in a year. Month-on-Month differences for seasonal and annual prices below are understated this month as the front season has moved from Summer 25 to Winter 25.

Month End Prices

Spot Prices

| Fuel | Apr-25 (p/kWh) | Mar-25 (p/kWh) | Month-on-Month Difference |

|---|---|---|---|

| Gas (NBP) | 2.59 | 3.34 | -22% |

| Power (UK Baseload) | 7.50 | 8.79 | -15% |

Front Months

| Fuel | Apr-25 (p/kWh) | Mar-25 (p/kWh) | Month-on-Month Difference |

|---|---|---|---|

| Gas (NBP) | 2.64 | 3.33 | -10% |

| Power (UK Baseload) | 7.00 | 8.63 | -19% |

Front Season

| Fuel | Apr-25 (p/kWh) | Mar-25 (p/kWh) | Month-on-Month Difference |

|---|---|---|---|

| Gas (NBP) | 3.00 | 3.37 | -11% |

| Power (UK Baseload) | 8.05 | 8.21 | -2% |

Annual Price (Apr-25)

| Fuel | Apr-25 (p/kWh) | Mar-25 (p/kWh) | Month-on-Month Difference |

|---|---|---|---|

| Gas (NBP) | 2.88 | 3.51 | -18% |

| Power (UK Baseload) | 7.41 | 8.57 | -13% |

Historical Comparison

| Fuel | 2019 Average Front Season Price (p/kWh) | % Increase to Apr-25 |

|---|---|---|

| Gas (NBP) | 1.64 | 83% |

| Power (UK Baseload) | 5.10 | 58% |

Outlook

The bullish summer outlook is slowly shifting as warmer weather and expected loosening of storage targets is leading to a more positive outlook. Prices for the remaining months of Summer 25 are now cheaper than Winter 25 contracts which should incentivize injections improving the storage position heading into winter.

Bearish Signals

- Potential positive outcome to Russia/Ukraine peace talks.

- Warmer weather expected to reduce residential demand.

- Expected loosening of storage targets.

Bullish Signals

- Low storage levels.

- Lower imports from Norway due to maintenance.

Want the best energy and water contracts for your business?

Ginger Energy can help you.

We take the time to understand your needs and handle everything with the supplier on your behalf. Throughout the entire life on your contract, we’re always on hand to help. And, there’s obligation to stick with us – you contract directly with the supplier, not with you..

Get in touch today to start saving money and time spent on finding the best business energy deals.